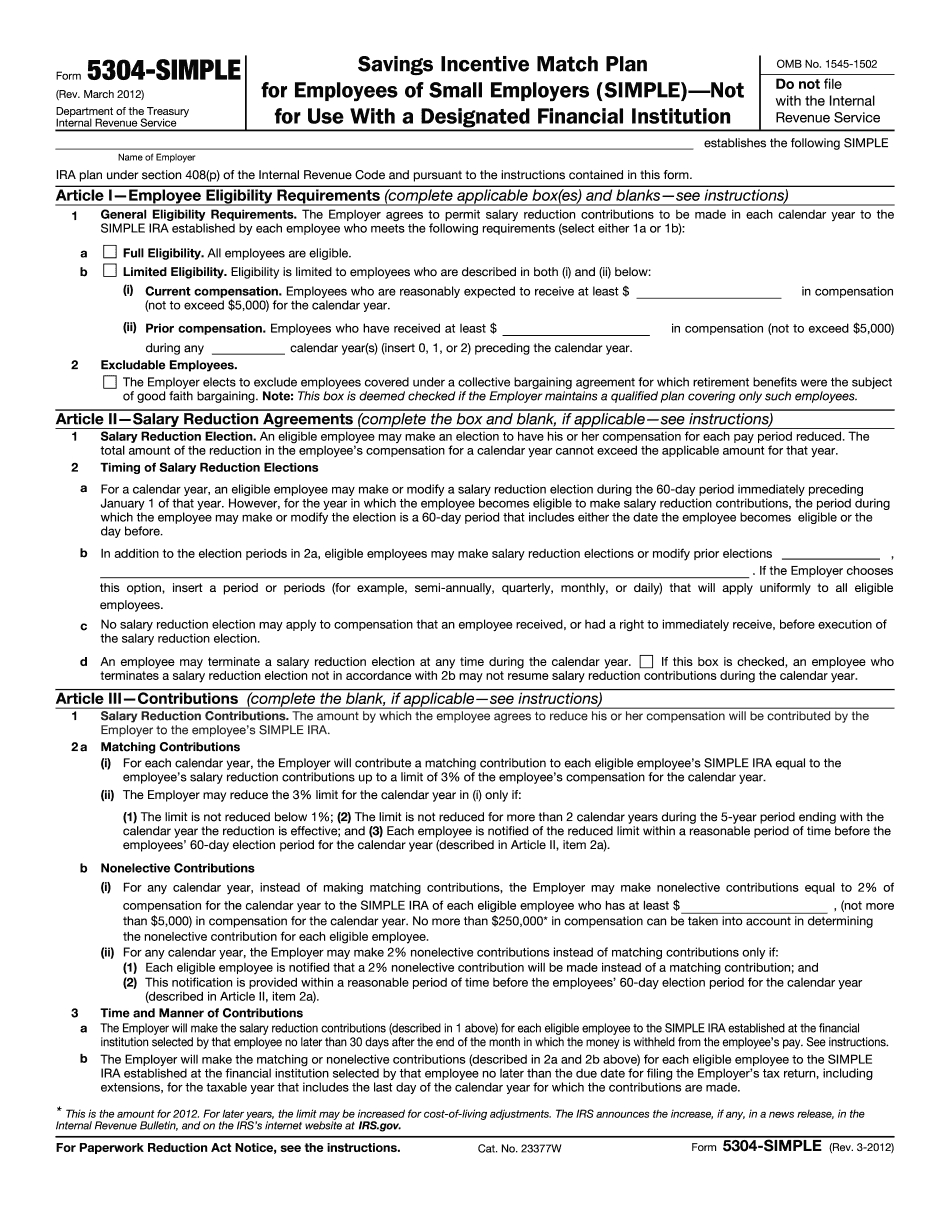

Music. Hi, I'm Michael Ruger. I'm a certified financial planner and the managing partner of Greenwich Financial Group. Today, I'll be discussing simple IRA plans with you. Simple IRA plans are a type of employer-sponsored plan that is commonly used by smaller companies. In many scenarios, such as for startup companies, the owners want to establish a plan for their employees while still investing money in the business. Simple IRA plans work well in these situations because they have lower costs compared to 401(k) plans. Additionally, employees are able to contribute to the plan from their own pay, and there is also an employer contribution. Another scenario where simple IRA plans make sense is when the employer believes that the contribution limits for simple IRAs, although lower than 401(k) plans, are sufficient for their needs. This allows them to provide a plan for their employees at a lower cost. To understand how simple IRA plans work, it is important to know that you must establish the plan by October 1st. Therefore, if it is already November in 2017, you cannot establish a plan for this year. New plan eligibility is different from 401(k) plans. In a simple IRA plan, you can cover just full-time employees. An employee is considered eligible for the plan if they earn at least $5,000 in compensation within a calendar year. This means that an employee who earns less than $5,000 is not considered eligible, but they do receive a year of service toward the simple IRA plan. One important aspect of simple IRAs is that employers have the option to exclude employees from the plan for up to two years. However, if desired, employers can be more lenient and allow employees to join the plan immediately, after six months, or after one year. Two years is the maximum period...

Award-winning PDF software

Video instructions and help with filling out and completing Why 5304 Simple Tax Form