Hello, my name is Kenneth Imbler Senior. Today, you're going to learn about the contribution rules behind a Simple Plan. This is not to be confused with an IRA asset or any other type of retirement plan because a Simple Plan is designed for certain benefits, but it's also designed with extra restrictions. First, if you have earned $5,000 in at least the last two years with your employer or you have the expectation that you are going to earn at least $5,000 in the next year, you are eligible to contribute to your Simple Plan. Now, here's a catch though -- you have to make sure that you do not contribute more than eleven thousand five hundred to your Simple Plan. Secondly, if you have another type of employer-sponsored program, then again that could be a SEP, it could be an employer-sponsored IRA, it could even be a 401k, 403 B, 457. You have to make sure that your total contributions to all retirement plans do not exceed sixteen thousand five hundred in 2012. Now, every year, hopefully, the government will index that up according to what they estimate inflation will be, but currently, it's sixteen thousand five hundred. It's your responsibility to make sure that you are not exceeding that total of all retirement plans. If you incur a penalty, you can't go back and say the employer should have known. The government puts that responsibility on you. The second catch with a simple program is, as you probably know, many programs can be rolled from one plan to another plan. So, you can roll an IRA to an IRA, you can roll a SEP to an IRA or the other way around. You can even roll your IRA into your 401k at work. But, you cannot roll your...

Award-winning PDF software

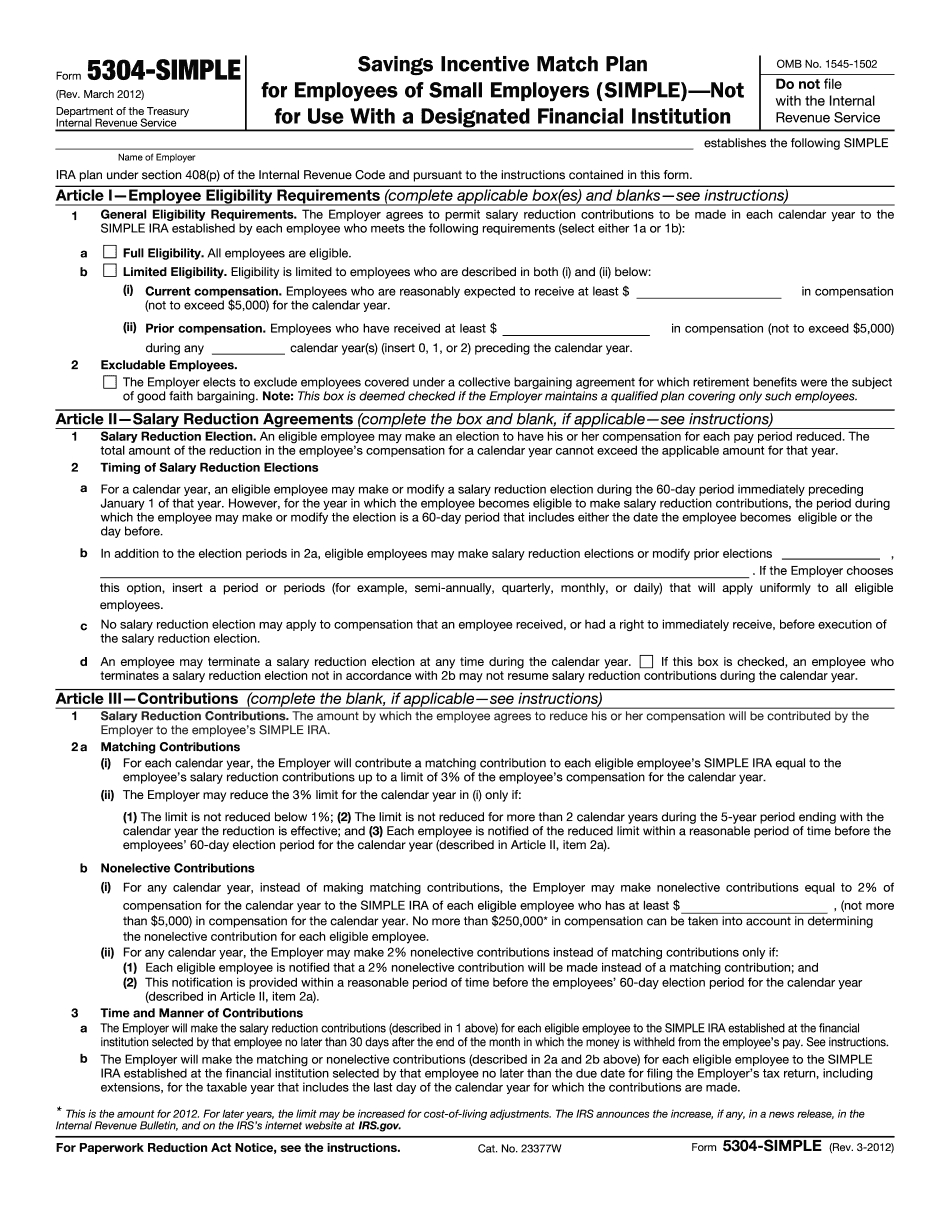

Simple ira Form: What You Should Know

SIMPLE IRA Plans for Employees A SIMPLE (Savings Incentive Match Plan for Employees of Small Employers of) plan offers great disadvantages for employees that have to make their first payroll or make a change in payroll before the year is over. It is also a disadvantage for employees who have to contribute to an IRA in order to make a retirement payment. However, if you are looking for a great alternative to the traditional 401(k) plan, SIMPLE IRA can be a great alternative for you or your employees. In addition, if you have to go through IRS forms in order to set up your Simple IRA Your employee must establish or sign an Employee Written Agreement (available at Fidelity.com and a certified copy of the Form W-4, Wage and Tax Statement). The agreement may be formalized by the employee or completed with an accountant. The agreement must state: 1. The employee's name 2. His or her current or former Employer 3. Current Employee or Former Employee 4. Current or Former Employees 5. Current Salary and/or Payroll information 6. Current retirement account interest 7. Minimum or maximum SIMPLE IRA allocation 8. Current retirement account withdrawal restrictions 9. What benefit is to be expected under the plan 10. Any applicable employee provisions 11. A list of the company's policy on SIMPLE IRA contribution distributions 12. A list of any company requirements related to employment termination 13. All tax implications such as Form 2555, Statement of Employee Rights, for each employee 14. In addition, the employee's last name 15. The employee's Social Security number (SSN) and date of birth 16. The employee's tax-exempt income. The employer must send a copy of each form (W-4, W-3 and W-2) to the employees. If there is a dispute over the employer's employee form, the question of whose information should be given to the employee will be decided by an insurance company or independent underwriter. Employee Written Agreement to Employer (PDF) for SIMPLE IRA Contribution Form. The agreement may be formalized by a lawyer, accountant or other legal representative of the employee or completed by the employee (provided the individual completing the agreement holds a valid private attorney license and is competent to serve as the employee's representative).

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5304-SIMPLE, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5304-SIMPLE online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5304-SIMPLE by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5304-SIMPLE from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Simple ira