Today we're gonna talk about the Simple IRA. If you're a small business owner that wants to reduce taxes, offer a retirement plan, increase employee retention, and control costs, this video is for you. If you're new to our channel or haven't subscribed, be sure to click on the bell at the bottom. My name is Travis Sickles, a certified financial planner with Sickled Hundred Financial Advisors. The Simple IRA stands for Savings Incentive Match Plan for Employees Individual Retirement Account. It is one of the simplest retirement accounts to open for your small business, as there are only two filing documents required: the 5305-Simple or the 5304-Simple. These need to be filled out in order to start the plan. The contributions to a Simple IRA are pre-tax, meaning they will reduce your overall tax liability as an employer or an employee. If you're under the age of 50, you can contribute up to $12,500. If you're 50 or older, you can contribute an additional $3,000 as a catch-up contribution, making a total of $15,500 for 2018. When it comes to employer contributions, the Simple IRA offers two options. The first option is the 2% non-elective contribution, which means the employer will contribute 2% of the employee's salary regardless of whether the employee contributes or not. For example, if the employee makes $50,000 and the employer has a 2% non-elective contribution, the employer will contribute $1,000 annually. The second option is the 3% elective contribution. For the employer to contribute an additional 3%, the employee must also contribute to the plan. The maximum contribution in this case would be 3% of the employee's salary. For example, if the employee is making $50,000 and contributes 3%, which is $1,500, the employer would also match 100% of that 3% by contributing another $1,500. If the employee contributes...

Award-winning PDF software

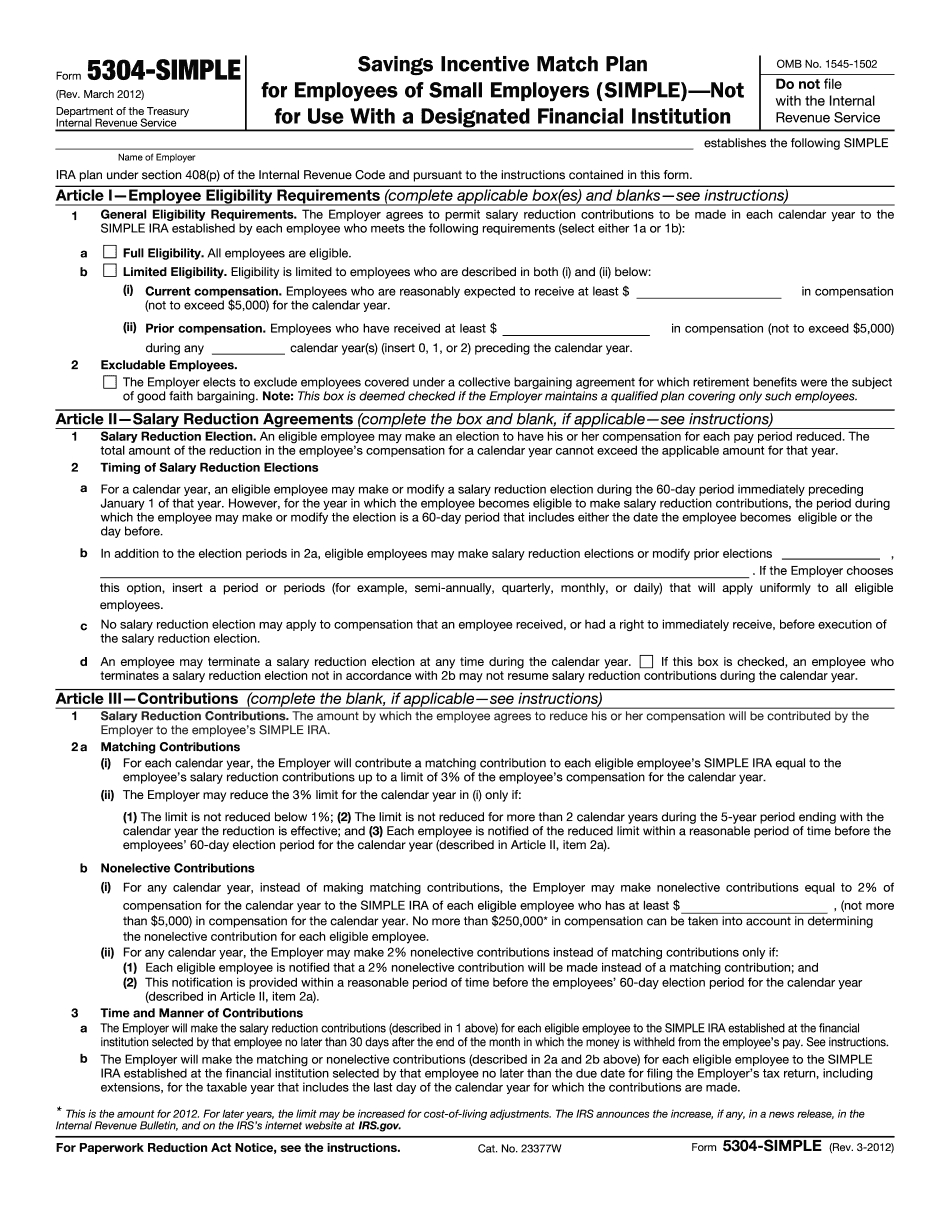

Simple ira 2025 Form: What You Should Know

Form 8949 is a report created by the IRS, is generally used by the IRS to pay the IRS for collecting tax payments. Because if you want to withdraw money from your SIMPLE IRA, it must be done through a tax professional who agrees to report your withdrawal to the IRS via Form 8949. So you must do your own taxes first, which is fairly low and the process, while not quite foolproof, is fairly straightforward. If you aren't sure you are eligible to cash out at a tax professional, please feel free to contact us. ∎ The IRS rules for an individual's SIMPLE IRA withdrawal do not change with your tax form (1099-R). You pay taxes on the amount of money you withdraw, which in this case is the full amount of money you have set aside. Therefore, if you have over-contributed through Roth IRA, traditional IRA, or SEP-IRA, the value of the money you have set aside on your SIMPLE IRA will be taxed. For example, in order to withdraw 25,000 from your Traditional IRA (50,000 if you're 50+), you would still have to pay taxes on 25,000, not the value of the tax-free IRA withdrawals. In this situation you would only have to pay the tax of the balance due, and you do not Roth IRA contributions are tax deferred. These are the tax-deferred portion of a traditional IRA which can only be withdrawn once the Roth IRA account has been opened. They are not taxed if you take out money in a taxable account. They are, however, taxed if you withdraw money in a taxable account and your Roth IRA is less than six years old. Thus, your Roth IRA is more valuable to the IRS than cash that is withdrawn for a retirement in retirement. (See also IRS Notice 2007-31) If you want to withdraw your SIMPLE IRA money, you may do so as a penalty or for a specific financial purpose or in contributions to a Roth. There are two ways to withdraw your SIMPLE IRA money.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5304-SIMPLE, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5304-SIMPLE online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5304-SIMPLE by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5304-SIMPLE from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Simple ira 2025