Hey, Dustin Tibbets here, a financial adviser with Jazz Wealth Managers. How are you doing today? I hope everything is good with you. I want to talk about making a financial plan, and I don't want to make this boring. A lot of people talk about making financial plans, and it becomes this long, drawn-out process. We have to write everything down on pieces of paper, check our expenses, and see where all our money is going. But it doesn't have to be that complicated. I want to go over four different things that we can do to start and build this financial plan, and I want to do them in order because I think this is important. The first part of any good financial plan is knowing where your money goes. While most people would say you need to create a budget, I totally think that's wrong. If you're not excited about making a financial plan or you have no idea where to get started, how are you supposed to sit down and figure out where all your money is going? At Jazz Wealth, we tell all of our clients to watch their money for a while. Give it 30 days, maybe even a little bit longer. While you're doing that, we offer a product called Nest Egg, completely for free. When you link your bank accounts, it will track your spending for you. You can customize it and add little notes if you like, but basically, it does the work for you. It's kind of like Mint, but we don't sell your personal information, and you won't receive any advertisements from us. But that's just the starting point. The Nest Egg that we have is actually a full financial planning software. We can help you with everything from your child's...

Award-winning PDF software

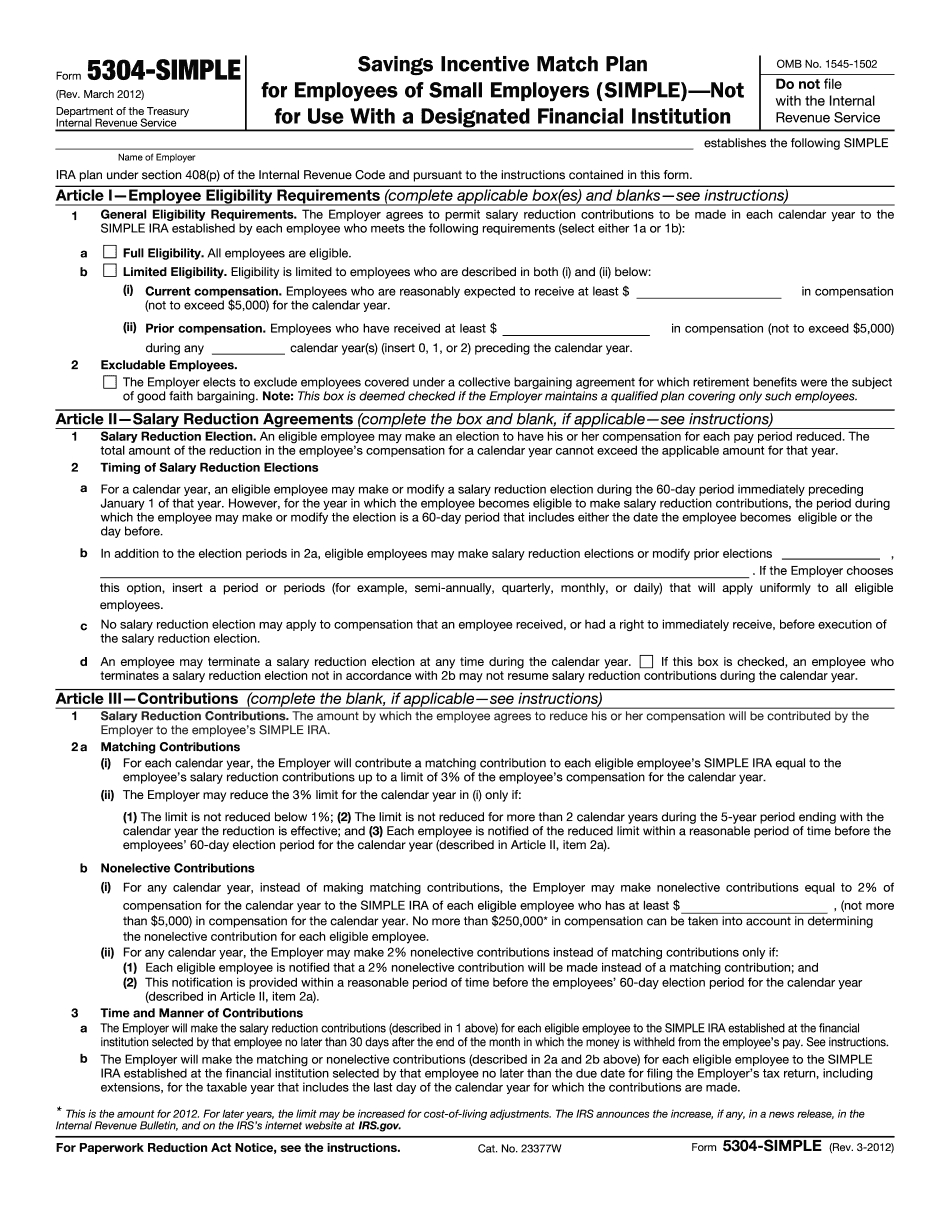

Simple ira roth Form: What You Should Know

No Time Limit Is a Good Option Under Certain Circumstances Apr 16, 2025 — Under some circumstances, a taxpayer may be able to contest an assessment of back taxes from time to time. IRS audits generally IRS Statute, Statute Of Limitations and Time Limits for Assessments of Statute of Limitations July 29, 2025 — For example, in general, the statute of limitations is 10 years for criminal violations and 10 years for civil violations or fraud, even if the return was not filed or paid. How long does it take to collect on a statute of limitation Sep 19, 2025 — Under the Statute of Limitations for the assessment of tax, the IRS has until the following payment day to assess the return or otherwise bring a proceeding for collection. The When do statute of limitations period start to run Mar 1, 2025 — In general, the statute of limitations begins to run when the assessment or notice is made, and it is mailed to you.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5304-SIMPLE, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5304-SIMPLE online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5304-SIMPLE by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5304-SIMPLE from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Simple ira roth