Today, I'm going to talk about the Roth IRA investment options. However, it's not just about the options or choices inside the Roth IRA; it's really about getting the Roth IRA to work as hard as possible for you. If this is your first time at our channel or you haven't subscribed, please click on the subscribe button at the bottom. My name is Travis Sickles, a certified financial planner with Sickles and/or Financial Advisors. So, the first thing we want to know is how the Roth IRA works. The Roth IRA is a type of account where you can put your securities, such as stocks, bonds, mutual funds, or ETFs. The money you put into the Roth IRA is after-tax, meaning it has already been taxed. For example, let's say you earn a dollar and 15% is taken out for taxes, leaving you with 85 cents. This 85 cents goes into the Roth IRA, and if it doubles over a chosen time frame, it becomes a dollar 70. The growth of this 85 cents can come out tax-free, along with the initial 85 cents. After reaching age 59 and a half, the full dollar 70 can be withdrawn without any tax consequences. However, if you withdraw the growth before reaching retirement age, it may be taxable with a 10% penalty. Therefore, it is advisable not to take out the growth before age 59 and a half. When we hear "tax-free," we often think it's a good thing because we want to pay as little in taxes as possible. However, it's important to understand that a Roth IRA does not reduce your tax liability today. That's where traditional IRAs and 401ks come in as they reduce your taxable income currently. The Roth IRA helps in reducing taxable income in retirement. Although there's...

Award-winning PDF software

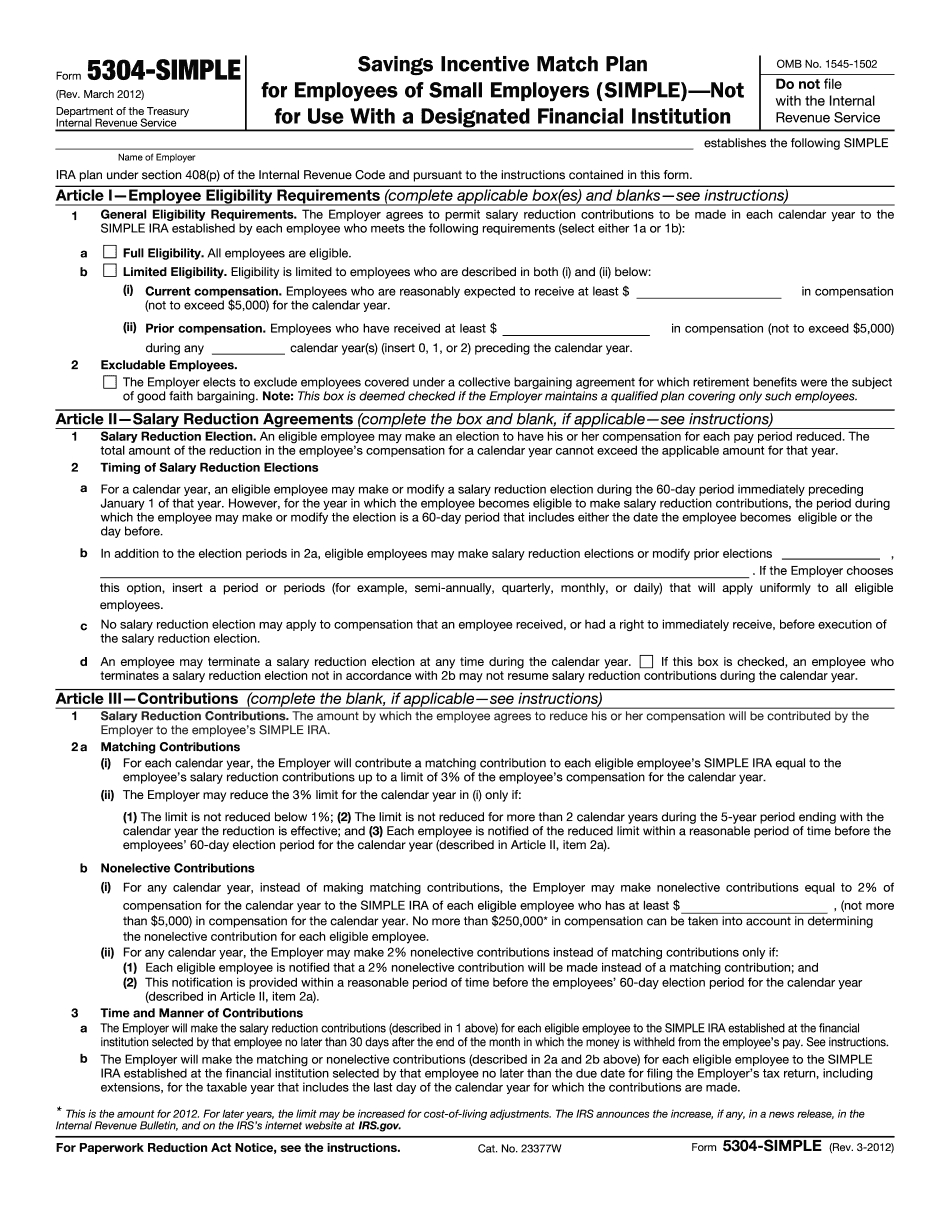

Simple ira investment options Form: What You Should Know

SIMPLE IRA Contribution Transmittal Form — Fidelity will mail this form and request additional information for employees. However, if you have already filed your SIMPLE IRA Contribution Transmittal Form — Schwab, you will need to file the Schwab contribution by mail in order for your payment to be processed SIMPLE IRA Contribution Transmittal — TD Ameliorate Note: All the required forms must be complete and signed by the plan participant. The plan participant must enter the password for the Diversified ETF Series (see this article for more information on the Diversified ETF Series) or ETF Series with Fidelity Investment Management and Diversified Portfolio (see this discussion for more information on the Diversified Portfolio) SIMPLE IRA Contribution — Vanguard will make contributions by mail. SIMPLE IRA Contribution Tax Form – NFL You will need a copy of this form (I think it's the one for the IRA) and a copy of your Vanguard IRA Statement of Operation (see this article for more information on the Vanguard Account Statement) If you want automatic payments, do not complete the form completely. Complete the last three pages and attach two copies of the Statement of Operation. The first copy should be given to your plan administrator. The second should be given to the payment provider on your behalf. Note: If you have already filed your SIMPLE IRA with TD Ameliorate (see the article on Simple IRA's), you would need to complete all portions. The two statements must be signed by yourself. Simpler IRA Plan — RED You will need your SIMPLE IRA Form I-401(K) at your workplace, your employer's social security number, or a valid Social Security number. You can use your driver's license to do this. All of your SIMPLE IRA Fund Statement(s) should also be on this form. RED has simplified the process and a very simple tax form. Once the form is completed by you, you get all the tax forms and your information sent to RED. The RED tax form has been approved by the IRS as a simplified version of the IRA Form T-2. This tax form is what you must file with the IRS. See the IRS site for more information: IRA: IRA Notice 790.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5304-SIMPLE, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5304-SIMPLE online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5304-SIMPLE by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5304-SIMPLE from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Simple ira investment options