Hello everybody. I know it all, Paul. This week's episode, I'm going to show how you, business owners, can save some money on your taxes and reward your employees at the same time. It's called a Simple IRA. It's designed for companies with less than 100 employees. Now, as a worker, have you ever felt like that person that keeps passing cake around and you don't get any? Well, don't worry, everyone is included in a Simple IRA. It's a great perk to you and tax-deductible to the business. Now, as a business owner, you can open a Simple IRA for your employees at a bank, insurance company, or investment firm. You can do it in person or online. Almost any kind of investment can go inside their annuities, bonds, CDs, mutual funds, and stocks. Now, you have to open the Simple IRA between January 1st and October 1st, unless you're a new business that started after that. You have to put in a 2% contribution for every eligible employee or you have to match their contributions up to 3% of their compensation. Now, as a company, you can change this amount each year, but you have to do the same percentage for every employee, and every employee is 100% vested automatically. Now, to be eligible, an employee has to have earned $5,000 for any of the previous two years and expects to earn another $5,000 in the current year. Now, for the employee, the money grows tax-deferred. It's never been taxed before, so once they cash out at retirement, it will be taxed then. The full retirement age is fifty-nine and a half years. If you cash out before then, you're going to be taxed and penalized 10% because it's supposed to be for retirement. Any money in the...

Award-winning PDF software

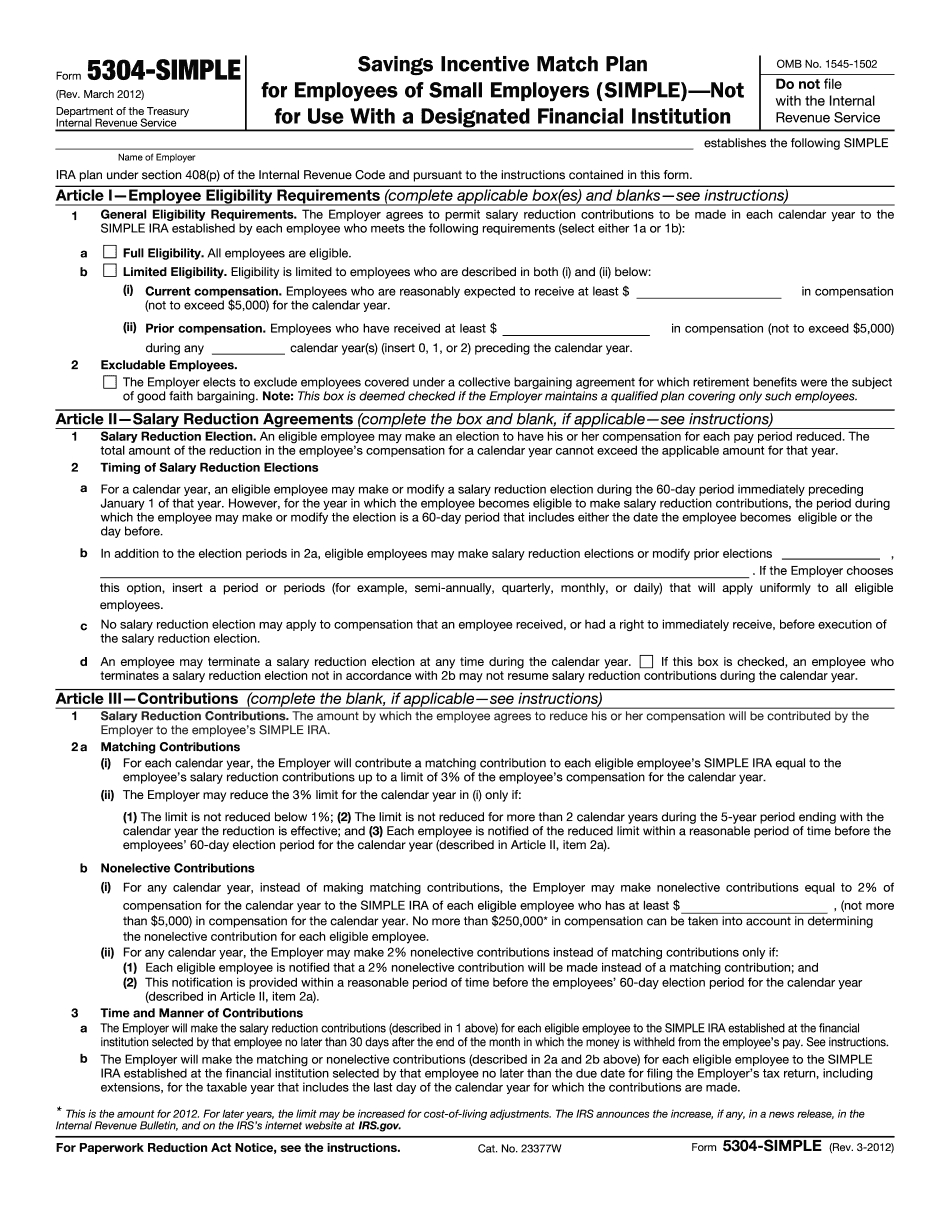

Simple ira vs 401k Form: What You Should Know

Read this article to find out if the SIMPLE IRA plan might work better for your business. How to Get Employees to Save in a SIMPLE Retirement Account and Use the Retirement Plan Jan 12, 2019 There are different ways to get your employees to save for retirement. And it's probably going to be a very big decision for you and your business. Whether you think that there are a huge number of employees who can benefit from a SIMPLE IRA, or whether you think there is just one person in your office who is willing to save for retirement, it's important to do a good job of setting expectations and making it clear to your employees about the consequences of not saving for retirement. You can do that by answering a few questions about the benefits and the drawbacks of an IRA. You'll also need to ask yourself whether you can count on the employee to have access to his or her retirement savings account. If you answer no to either of these, this is not a plan to consider implementing. IRA vs. 401(k): Which Is Right for Your Business? — SmartAsset.com May 13, 2018, Most businesses, if they can manage their 401(k) plans for the last several years, should have a plan in place that is able to keep up with their business's needs, while their IRA offers some benefits but requires the flexibility to adapt over time. But how long do your business and workers need to wait before they're taking full advantage of what the 401(k) plan offers? Read this article to learn more about the average time to retirement and make sure you have a plan in place for the future. IRA vs. 401(k): Which One Is Right for You? — SmartAsset.com May 13, 2018, The 401(k) plan is an important part of many businesses' retirement plans. But some business owners may be wondering which one is better: the SIMPLE IRA or the 401(k)? This article will help you compare the two. IRA: A Smart Investment Choice for Business Owners — SmartAsset.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5304-SIMPLE, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5304-SIMPLE online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5304-SIMPLE by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5304-SIMPLE from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Simple ira vs 401k